For years the Small Business Super Clearing House (SBSCH) was the quiet default for small employers: free, government-run, and good enough for quarterly super. It closes on 30 June 2026 — the day before Payday Super begins. For accounting practices, that turns a routine tool retirement into a migration project with a hard deadline.

This briefing covers who is affected, what the alternatives are, and how to move clients across without anyone missing their first 7-business-day deadline.

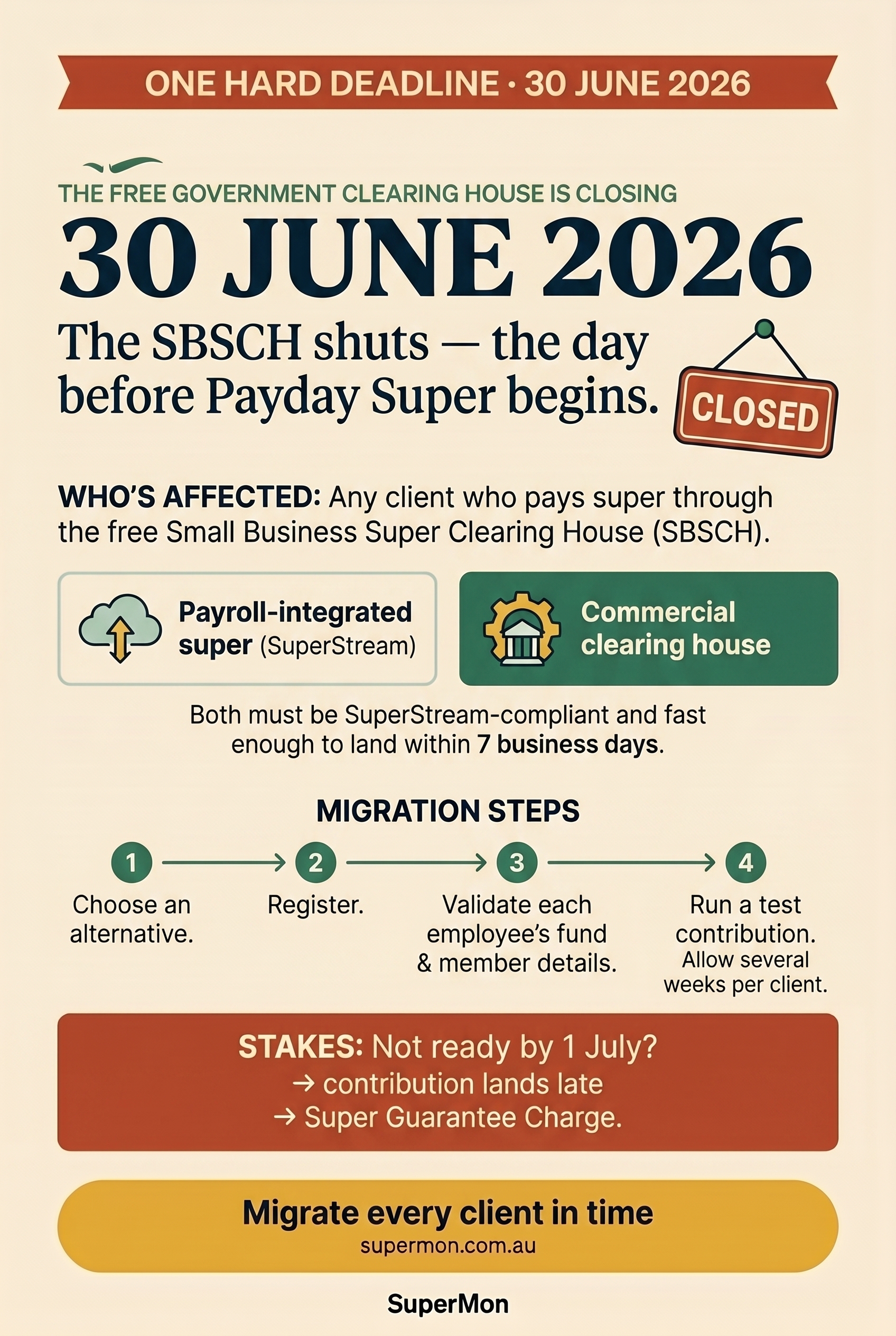

What is changing, and when?

The SBSCH stops accepting contributions from 30 June 2026. The next day, 1 July 2026, Payday Super's 7-business-day rule takes effect. The two events are deliberately back to back: the old free clearing house was designed for a quarterly world, and the new rules need infrastructure that can move money to funds within days of every payday.

So two things change at once for affected clients — the tool they pay super with, and the deadline they pay it by. Handling them together, late in June, is where practices get caught.

Which clients are affected?

Any client who pays super through the SBSCH needs to move. In practice that is heavily weighted toward:

- Small employers with up to 19 staff, or under $10 million in annual turnover, who qualified for the SBSCH.

- Clients you onboarded years ago and never migrated to payroll-integrated super.

- Businesses that pay super manually each quarter rather than through automated payroll.

Start by running a list of every client and how they currently pay super. The ones flagged "SBSCH" or "manual" are your migration list.

What are the alternatives to the SBSCH?

There are two mainstream replacements, and both must be SuperStream-compliant:

| Option | Best for | What to check |

|---|---|---|

| Payroll-integrated super | Clients already on Xero, MYOB, or similar | That auto-super is enabled and processing time fits inside 7 business days |

| Commercial clearing house | Clients not on integrated payroll, or with many funds | Fees, SuperStream compliance, and settlement speed |

For most clients on modern payroll software, enabling the software's own super payment feature is the cleanest path — it keeps payroll and super in one system and shortens the gap between payday and the fund receiving the money.

A step-by-step migration plan

Work through this per client, finishing well before their first July payday:

- Inventory. List every client paying via the SBSCH and note their pay frequency. Weekly and fortnightly payers face the tightest deadlines and should migrate first.

- Choose the replacement. Default to payroll-integrated super where the client is already on supported software; otherwise select a commercial clearing house.

- Register and connect. Set up the new method, authorise it, and link it to the client's bank account and default fund.

- Validate fund details. Confirm member numbers and stapled-fund information for every employee. Stale details are the most common cause of rejected or delayed contributions.

- Run a test contribution. Process one real or trial payment and confirm it reaches the fund inside 7 business days. Measure the actual settlement time so you know your real buffer.

- Document the cutover date. Record the last SBSCH payment and the first payment on the new method so nothing falls through the gap between systems.

Why timing is the real risk

The SBSCH closure is not technically hard. The danger is the calendar. Every client you leave until late June is a client switching payment systems in the same fortnight the deadline rules change. If the new clearing house is not fully working — an unverified fund, a slow first settlement, a missing authorisation — the contribution is late under Payday Super, and the Super Guarantee charge can follow.

Finish migrations before 1 July 2026, then use the first few July pay runs to confirm every client's contributions are landing inside the 7-business-day window. Treat the early July paydays as a monitoring period, not a set-and-forget switch.

Turning the deadline into a client conversation

The SBSCH closure is also a reason to reach out to every affected client now. A short note explaining that their free clearing house is closing, that you are moving them to a compliant alternative, and that you will be watching their new deadlines positions the practice as proactive rather than reactive.

It is the natural lead-in to ongoing Payday Super monitoring — the work of confirming, every pay cycle, that each client's super arrived on time. That continuous oversight is exactly what the old quarterly clearing house never required, and exactly what the new rules now demand.