Most conversations about Payday Super frame it as a burden: a new deadline, a higher risk of penalties, more to watch. That framing is accurate, and it is also an opportunity. A continuous obligation on every client is, from a practice's point of view, a continuous service you can deliver and bill for.

This briefing lays out how to turn Payday Super monitoring from unbilled compliance overhead into a productised, recurring-revenue line.

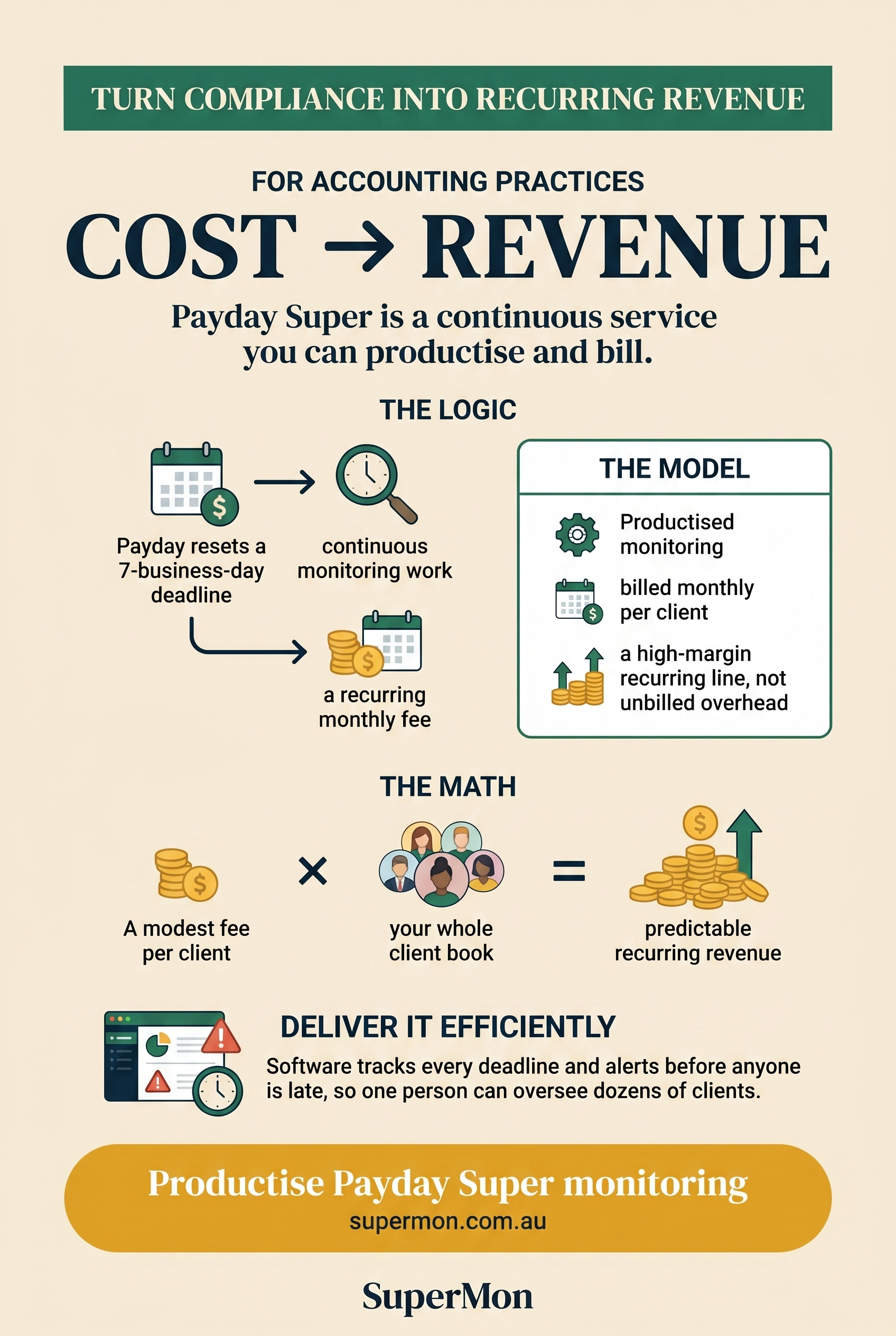

Why Payday Super is a recurring-revenue opportunity

Quarterly super was periodic, so it was hard to charge for as an ongoing service — four events a year blur into general compliance work. Payday Super is different in a way that matters commercially: the obligation recurs on every payday, for every client, indefinitely.

That continuity is what makes it billable as a recurring service. The work is no longer "lodge super four times a year"; it is "confirm, every pay cycle, that each client's super landed within 7 business days." Ongoing work supports an ongoing fee.

What clients are actually paying for

Clients are not paying for data entry. They are paying to not think about a deadline that now carries a non-deductible penalty and resets constantly. The service you are selling is peace of mind, backed by proactive monitoring:

- A standing watch on every payday's 7-business-day deadline.

- An alert before a deadline is missed, not a report after.

- A clear record that contributions arrived on time, in case the ATO ever asks.

Framed that way, the value is obvious to the client. One avoided Super Guarantee charge — and the awkward conversation that comes with it — pays for the service many times over.

How to package it as a service

The cleanest model is a productised monitoring service billed monthly per client. A simple three-tier structure works for most practices:

| Tier | Scope | Typical client |

|---|---|---|

| Monitor | Deadline tracking and alerts | Stable clients on regular pay cycles |

| Monitor + nudge | Alerts plus a prompt to the client to pay | Clients who run their own payroll |

| Managed | Monitoring plus you handle the payment workflow | Clients who outsource payroll to you |

Put the service on your engagement letter as a named line, not buried in general compliance. Naming it makes it billable, makes the value visible, and gives the client something concrete to say yes to.

A worked example

The economics are straightforward. Take a practice that bills monitoring at a modest per-client fee:

- Bill 30 clients at $49 per client per month → $1,470 per month in service revenue.

- Subtract the cost of monitoring software at, say, $299 per month.

- Net new margin: roughly $1,170 per month, or about $14,000 a year — from work the new rules already require you to do.

The numbers scale with your client base, and the marginal cost of adding a client to a monitoring tool is close to zero. This is why monitoring behaves like a high-margin recurring line rather than time-and-materials compliance.

A single missed Payday Super deadline can cost a client more in Super Guarantee charge than a full year of monitoring fees. That asymmetry is the entire sales pitch.

Delivering it without drowning in manual work

The catch is obvious: if monitoring 30 clients means manually checking 30 pay runs every week, the margin disappears into labour. The model only works if the watching is automated.

In practice that means software that:

- Connects to each client's payroll — reading pay runs from Xero or similar with read-only access.

- Tracks every payday's 7-business-day deadline automatically, accounting for weekends and public holidays.

- Alerts the practice before a deadline is missed, so one person can oversee a whole client base by exception rather than by manual review.

With that in place, the human effort per client drops to handling the occasional alert, while the fee per client stays the same. That gap between flat effort and recurring revenue is the margin.

Where to start

You do not need to roll this out across the whole book at once. Start with the clients who carry the most risk — weekly and fortnightly payers, and anyone migrating off the Small Business Super Clearing House before it closes on 30 June 2026. Offer them monitoring as a named service, price it against the penalty it prevents, and use the early results to extend the offer to the rest of your clients.

Payday Super is going to demand this work whether or not you charge for it. The only real decision is whether it sits on your engagement letter as a revenue line, or on your team's plate as unbilled overhead.