Payday Super is the biggest change to Australia's superannuation system since the Super Guarantee began. For most employers the mechanics are simple to state and easy to get wrong: super now follows payroll instead of trailing it by months.

This guide covers what changes on 1 July 2026, the 7-business-day rule in detail, what happens when a payment is late, and a short checklist to run before the first compliant payday.

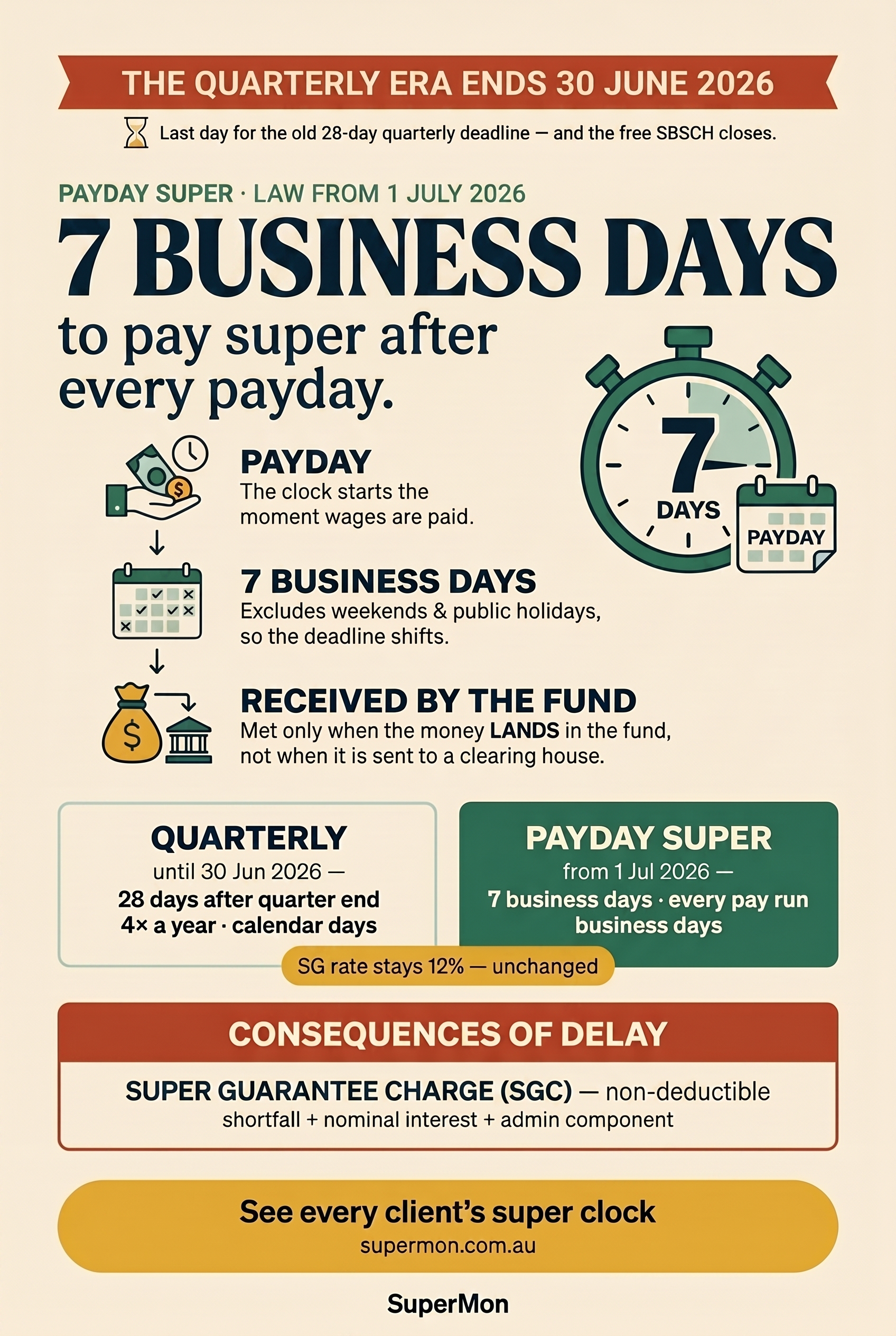

What is Payday Super?

Payday Super is a reform requiring employers to pay Super Guarantee (SG) contributions at the same time as wages, rather than quarterly. From 1 July 2026, every time you pay salary or wages, the matching super must reach the employee's fund within a tight window measured in business days.

The reform exists because quarterly super made it easy for unpaid super to build up unnoticed. Aligning super with payday makes shortfalls visible almost immediately and gives employees their entitlements sooner.

When does Payday Super start?

Payday Super applies to qualifying earnings paid on or after 1 July 2026. Earnings paid up to 30 June 2026 still fall under the existing quarterly SG deadlines, so most practices will run both rules briefly across the changeover.

What is the 7-business-day rule?

Under Payday Super, an employee's super contribution must be received by their fund within 7 business days of the day you pay their qualifying earnings. Two details matter:

- Received, not sent. The deadline is met when the money lands in the fund, not when you submit it. Clearing-house and SuperStream processing time eats into your 7 days, so you cannot leave payment to the last moment.

- Business days, not calendar days. Weekends and national public holidays are excluded from the count. That means the actual calendar deadline shifts from one payday to the next depending on where holidays fall.

A weekly payroll generates a fresh 7-business-day deadline every single week. A practice managing dozens of clients on different pay cycles is tracking dozens of independent countdowns at once.

How is this different from the old quarterly system?

| Quarterly SG (until 30 June 2026) | Payday Super (from 1 July 2026) | |

|---|---|---|

| Deadline | 28 days after quarter end | 7 business days after each payday |

| Frequency | 4 times a year | Every pay run |

| Day counting | Calendar days | Business days |

| Visibility of shortfalls | Months later | Within days |

| SG rate | 12% | 12% (unchanged) |

The rate and the funds are identical. What changes is cadence: from four predictable dates a year to a rolling deadline that resets on every payday.

What happens if super is paid late?

A late payment triggers the Super Guarantee charge (SGC). The SGC is not deductible and is made up of the super shortfall, nominal interest on that shortfall, and an administration component. Because it is calculated on total salary and wages rather than ordinary time earnings, the charge can exceed the super you would have paid on time.

The ATO's compliance guideline PCG 2026/1 sets out a more supportive approach during the first year for employers who are genuinely trying to comply and who correct mistakes quickly. It is leniency in how the ATO engages, not an exemption: the obligation and the charge still apply. The practical takeaway is to fix any miss fast and keep evidence that your processes are sound.

What employers must do before 1 July 2026

Run this checklist with each client before their first post-1-July payday:

- Confirm your payment timing. Map how long money currently takes to travel from your bank to each fund via your clearing house. If it is close to or beyond 7 business days, change the process now.

- Replace the Small Business Super Clearing House. The free SBSCH closes on 30 June 2026. Anyone relying on it needs a SuperStream-compliant alternative — payroll-integrated super payments or a commercial clearing house — in place before then.

- Check default fund and stapling details. Late or rejected contributions often come from stale fund details. Validate member numbers and stapled-fund information ahead of the changeover.

- Diarise business-day deadlines, not dates. Because the deadline moves with public holidays, a fixed calendar reminder will drift. Track the 7-business-day window per pay run.

- Decide who watches the clock. Quarterly super was a periodic task. Payday Super is continuous monitoring. Assign clear responsibility, or use software that flags an approaching deadline automatically.

Does Payday Super change how much super I pay?

No. The Super Guarantee rate is 12% of ordinary time earnings, the same as it was the day before the reform. Payday Super changes when super is paid, not how much or how. Your default fund, your SuperStream messaging, and the contribution amounts all stay the same — only the timing tightens.

For an accounting practice, that single change is deceptively large. Quarterly super was four events a year you could plan around. Payday Super is a live obligation on every client, every pay cycle, with a deadline that quietly moves. The firms that handle it best are treating it as something to monitor continuously rather than reconcile after the fact.